Audi Car Finance

Audi Car Finance  BMW Car Finance

BMW Car Finance  Ford Car Finance

Ford Car Finance  Kia Car Finance

Kia Car Finance  Land Rover Car Finance

Land Rover Car Finance  Mercedes Benz Car Finance

Mercedes Benz Car Finance  Nissan Car Finance

Nissan Car Finance  Peugeot Car Finance

Peugeot Car Finance  Tesla Car Finance

Tesla Car Finance  Toyota Car Finance

Toyota Car Finance  Vauxhall Car Finance

Vauxhall Car Finance  Volkswagen Car Finance

Volkswagen Car Finance Understanding APR in Car Finance: What It Means and Why It Matters

Understanding APR in Car Finance

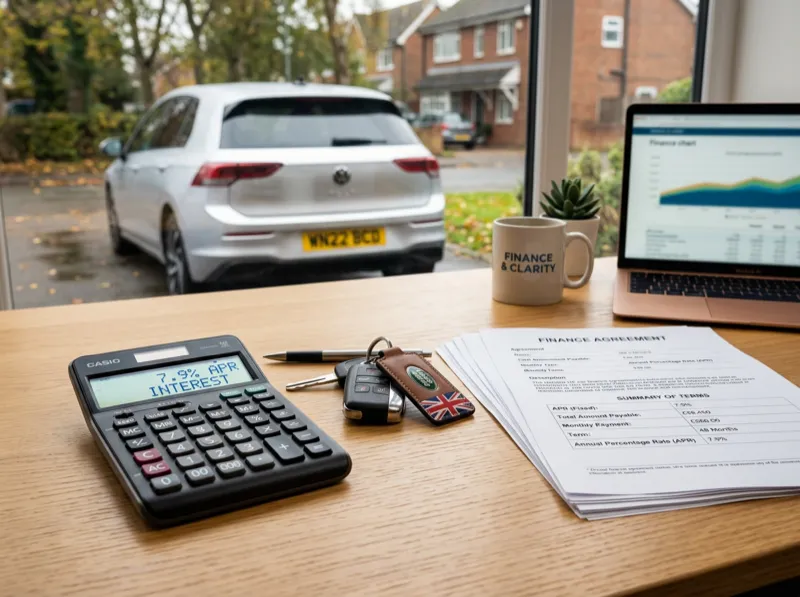

When you are shopping for car finance, you will see the term APR used frequently. It is one of the most important numbers to understand because it directly affects how much you pay for your car in total. Yet many people are unsure what APR really means or how to use it when comparing deals.

What Does APR Stand For?

APR stands for Annual Percentage Rate. It represents the total cost of borrowing expressed as a yearly percentage. Crucially, APR includes not just the interest rate but also any mandatory fees and charges associated with the finance agreement.

This makes APR a more reliable comparison tool than the flat interest rate alone, because it gives you a fuller picture of the true cost of the finance.

How APR Affects Your Payments

The APR directly influences how much you pay each month and how much you pay in total over the life of the agreement. A higher APR means more interest charged, which means higher monthly payments and a greater total cost.

For example, consider a car priced at fifteen thousand pounds financed over four years:

- At 7% APR, you might pay around three hundred and sixty pounds per month with a total interest cost of around two thousand two hundred pounds.

- At 12% APR, the monthly payment could rise to approximately three hundred and ninety-five pounds, with total interest approaching three thousand nine hundred pounds.

The difference of five percentage points in APR translates to a significant amount over the term of the agreement.

Representative APR vs Personal APR

When lenders advertise their rates, they are required to show a representative APR. This is the rate that at least 51% of successful applicants will receive. It does not mean everyone will get this rate.

Your personal APR will depend on several factors:

- Credit score: A higher credit score generally results in a lower APR.

- Income and affordability: Lenders want to know you can comfortably afford the payments.

- Deposit size: A larger deposit can sometimes secure a better rate.

- The car’s age and value: Newer cars may attract lower rates because they hold their value better.

- The finance type: PCP and HP may have different rates for the same vehicle.

- The lender: Different lenders have different risk appetites and pricing models.

Fixed vs Variable APR

Most car finance agreements in the UK use a fixed APR, which means your interest rate and monthly payment stay the same throughout the agreement. This provides certainty and makes budgeting straightforward.

Variable APR, where the rate can change during the agreement, is rare in car finance but more common with some personal loans. If you are comparing options, a fixed APR is generally preferable for the predictability it provides.

How to Compare APR Between Deals

When comparing car finance quotes, APR is the best single number to look at for a like-for-like comparison. However, keep the following in mind:

Compare like with like. Make sure you are comparing the same finance type (PCP with PCP, HP with HP), the same term length, and the same deposit amount. Changing any of these variables will affect the monthly payment regardless of the APR.

Look at the total amount payable. The APR tells you the rate, but the total amount payable tells you exactly how much the car will cost you over the full term. This is the figure that matters most to your wallet.

Consider the monthly payment. A lower APR with a shorter term may result in higher monthly payments than a slightly higher APR with a longer term. Make sure the monthly payment fits your budget.

Factor in any fees. While APR should include mandatory fees, check whether there are any additional charges such as option-to-purchase fees, arrangement fees, or early settlement penalties.

Why Your APR Might Be Higher Than Advertised

If you receive a quote with an APR higher than the representative rate, it is usually because of one or more of the following:

- Your credit score is lower than average

- You have a limited credit history

- You are borrowing a smaller or larger amount than the typical range

- The car you are financing is older or has higher mileage

- The lender has assessed your application as higher risk

This does not necessarily mean you are getting a bad deal. It simply reflects the lender’s assessment of the risk involved. Over time, as you build a positive payment history, you may be able to secure better rates on future agreements.

Can You Negotiate APR?

In general, the APR is set by the lender based on their assessment of your application. However, a broker like Happy Motor Finance can help by comparing offers from multiple lenders to find the most competitive rate for your profile. This is often more effective than trying to negotiate with a single lender.

The Bottom Line

APR is the most important number to understand when comparing car finance deals. It represents the true annual cost of borrowing and allows you to make meaningful comparisons between offers. Always check the total amount payable alongside the APR, and make sure the monthly payments are comfortable for your budget.

At Happy Motor Finance, we help you find the best APR available for your circumstances by comparing deals across our panel of lenders. Get a free quote today.

Happy Motor Finance

FCA Authorised (FRN 989250) · SAF Approved

Our team of FCA-authorised finance specialists help people across the UK get behind the wheel, regardless of credit history. We act as a credit broker, searching a panel of lenders to find the right deal for you.

Ready to Get Started?

Apply for car finance today and get a decision in minutes.

With no impact to your credit score*

We act as a credit broker, not a lender

Representative example: borrowing £6,500 over 5 years with a representative APR of 16.9%, an annual interest rate of 16.9% (Fixed) and a deposit of £0.00, the amount payable would be £161.19 per month, with a total cost of credit of £3,171.55 and a total amount payable of £9,671.55. This is an example only, lender fees may apply. The exact rate you will be offered will depend on your circumstances. All finance subject to status.

*After completing the application, lenders will perform a “soft search” that will not affect your credit score. Should you get an offer of finance and wish to proceed, the lender will then perform a “hard search” of your credit file. Finance acceptance is not guaranteed, please click the following link for more information: Initial Disclosure Document